On Wars, Interest Rates, Oil Prices, and Gold.

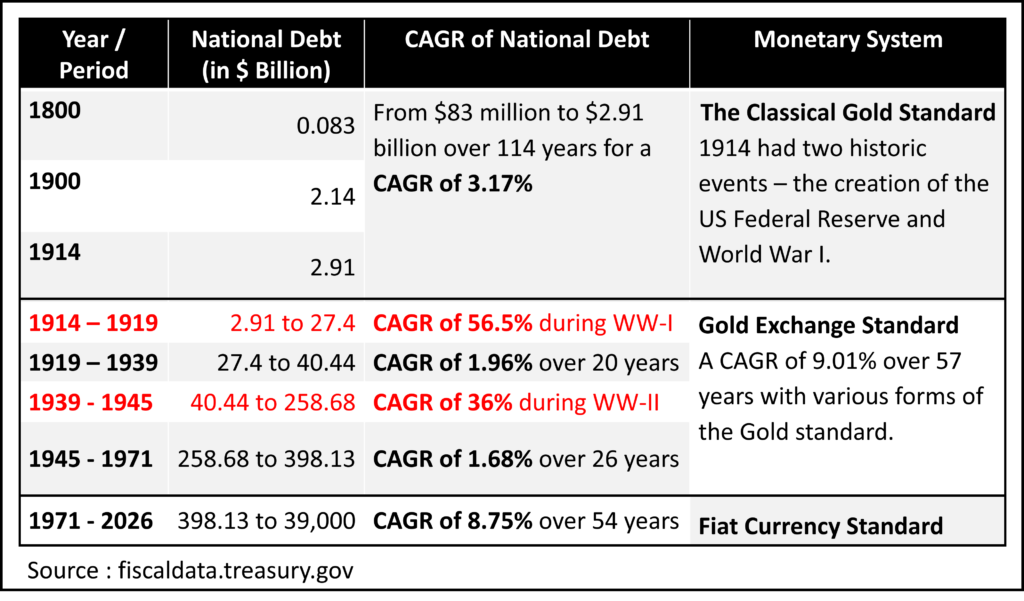

The last few weeks have been “different” to say the least. Just to list a few obvious ones: The US and Israel made an unprovoked attack on Iran. By the admissions of Trump’s own staff, Iran did not pose any material threat to the US at this point. More importantly, this escalation occurred while negotiations between the US and Iran were ongoing. The Straits of Hormuz have been closed, choking off nearly 20% of the world’s oil supply. In addition, there has been extensive damage inflicted by Israel to the South Pars gas field – the largest gas field in the world, which is jointly operated by Iran and Qatar. Extensive damage to countries that had US military bases, such as Bahrain, Qatar, Kuwait, the UAE, and Saudi Arabia. The invincibility of the US Army’s defence systems has pretty much been laid threadbare by Iran, so much so that even the mainstream media is speculating about the end of the Petrodollar. All these events should have caused gold prices to skyrocket and perhaps even cross $6,000/oz, and yet, what we witnessed was the exact opposite. Gold plummeted to just above $4,000/oz. Higher oil prices and the much higher-than-anticipated PPI (for Feb 2026, which came in at a monthly 0.7%) were the supposed triggers behind gold’s plunge. That, of course, is an extremely bizarre and almost child-like economic explanation for what happened. The antidotes follow. I. Wars and Higher Gold Prices The prevailing notion that wars cause gold prices to spike is indeed correct. For the wrong reasons, though. It is not for ...