in_tradingview65d ago

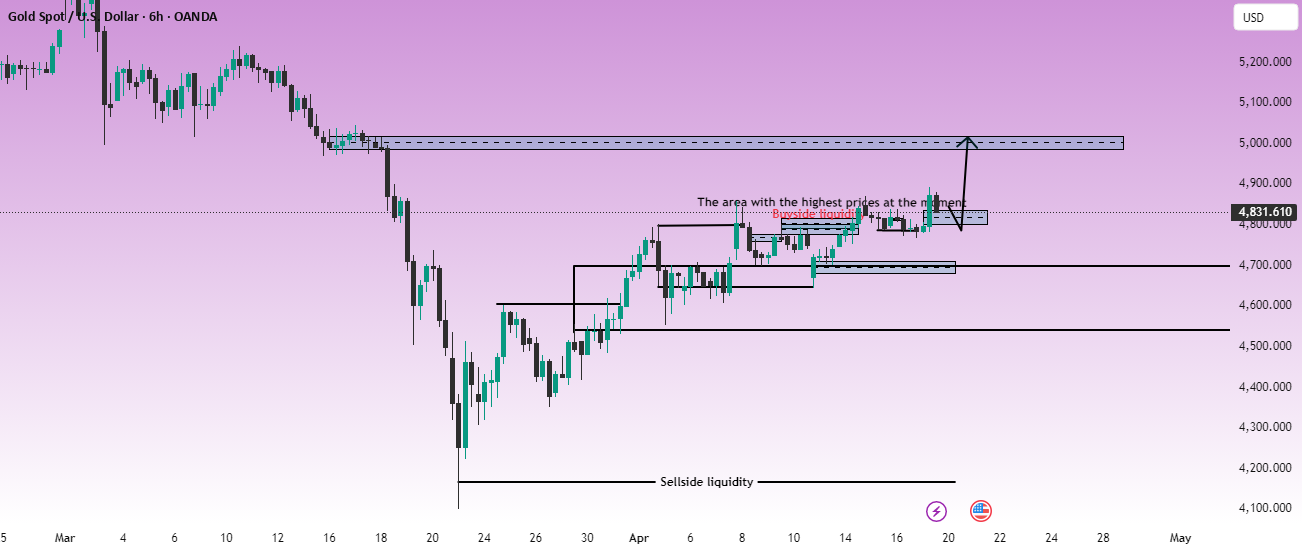

Gold Holds Firm Above 4,800 as Buyers Keep the Recovery Structure Alive XAUUSD is still trading with a constructive tone, even though the market is no longer moving in a clean impulsive leg. Gold remains supported above the 4,800 handle, and that matters. After the recent recovery, price is no longer trading from weakness. It is now trading from a position where buyers have already rebuilt part of the lost structure and are trying to keep control near the upper range. The fundamental backdrop also helps explain why gold is holding up. The latest headlines suggest that while the US-Iran talks did not produce a breakthrough, the broader tone is not one of full escalation either. That keeps the market in a cautious middle ground. At the same time, uncertainty around the Federal Reserve’s next moves continues to limit stronger US dollar momentum. When the dollar cannot gain clean upside traction, gold usually finds room to stay supported on dips rather than slipping into a full reversal. So this is not a panic bid. It is a market where support is holding because the bearish case is not strong enough to take control. Technical Structure From a technical perspective, XAUUSD is still trading inside a short-term recovery structure, but momentum has slowed under a familiar resistance band. The chart shows that price is rotating around the 4,780–4,820 region, which is acting as the current balancing area. Buyers have kept the market above the recent recovery base, but gold has not yet forced a clean breakout through the upper boundary. The key levels on the chart are clear: 4,780–4,820 is the current resistance and near-term decision zone 4,680–4,700 is the first important support area 4,560–4,585 is the deeper support zone if the current base weakens the higher upside path remains valid only if buyers continue holding the structure and reclaim the top range with conviction This means the market still leans constructive, but the upside is no longer automatic. Buyers need follow-through, not just support. Key Price Zones Immediate Resistance: 4,780–4,820 This is the current ceiling. If gold can reclaim and hold above it, the recovery gains another leg. First Support: 4,680–4,700 This is the first zone protecting the current structure. As long as price remains above it, the rebound stays intact. Deeper Support: 4,560–4,585 If the market loses the first support layer, this becomes the next important defensive zone. Market Scenarios Scenario 1 – Hold support and break higher This is the constructive scenario. If buyers continue defending the current base and push through the 4,780–4,820 cap, gold may extend the recovery and reopen the next upside path. Scenario 2 – Stay in consolidation This is also realistic. The market may continue moving sideways while waiting for a stronger macro trigger. As long as support holds, that would still look like healthy consolidation rather than weakness. Scenario 3 – Lose support and rotate lower If price breaks below 4,680–4,700, the recovery loses short-term momentum and the market may revisit the deeper 4,560–4,585 support zone before buyers attempt to stabilize it again. Market Insight Gold is in a better position than it was a few weeks ago, but the chart is now asking for proof. The recovery is real. The support is holding. But unless buyers clear the current ceiling, the market may stay in a controlled range rather than expand immediately into a stronger bullish leg. For now, the message is simple: XAUUSD is still holding recovery structure above 4,800, but the next move depends on whether buyers can finally turn support into a clean break through resistance.